Risk Management: Introduction to hedging tools (6)

Our final post in this series on the basics of bunker hedging will focus on another tool that offers executives a combination of risk reduction and flexibility.

#3: Collar

A collar (a combination of a call option and a put option) is a financial instrument designed to hedge a company’s fuel exposure by locking prices into a certain range. These products are often traded at zero upfront cost. However, depending upon the exact structure, a premium can be received.

Execution:

- Select the most relevant contract (e.g. US Gulf Coast No.6 Fuel Oil 3%)

- Select volume of fuel to hedge

- Select time period

- Select price cap level (or call strike price)

- Select price floor level (or put strike price)

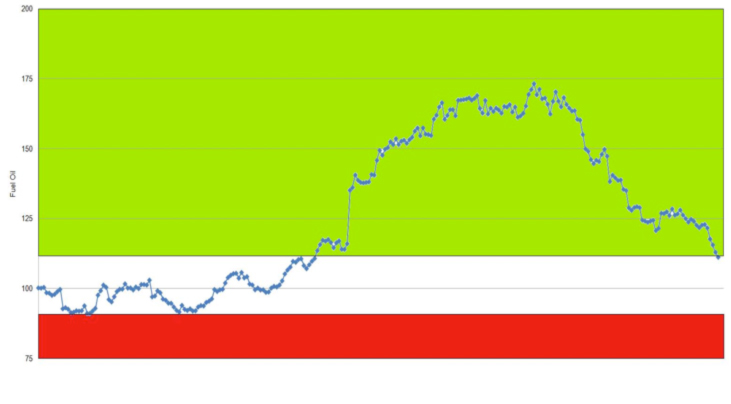

(This example uses Monte Carlo simulated data assuming 30% volatility and a Fuel Oil index starting at an execution price of 100.)

Scenario 1: Fuel price moves below the price floor level (red zone). The company makes a cash payment to its trading counterparty but this is offset by the lower physical fuel prices that it pays in the market. The company will benefit from falling prices until the floor is passed.

Scenario 2: Fuel prices remain between cap and floor levels (un-shaded zone). There are no further cash payments or receipts. Physical fuel is purchased in the market and the company is exposed to price fluctuations within the predefined range.

Scenario 3: Fuel price rises above cap level (green zone). The company receives cash from its trading counterparty to offset the higher physical fuel prices that it must pay in the market. The company will be exposed to rising fuel prices until the cap is passed.

By using a collar (we will assume a zero cost for this example), the commercial hedger has defined a range of prices within which his bunker price will be constrained over a particular time period. This structure is often used by companies who desire similar upside protection to a cap, but do not wish to pay a premium for this insurance against rising prices. By adding a floor into the structure, they receive a premium that allows them to finance the cap. While they retain some exposure to the benefits of falling prices, they forego the ability to take advantage a price drop beyond a certain level, in order to pay for their insurance against price spikes.

A collar is somewhat analogous with a bunker price adjustment clause in a COA or voyage charter-party. If a pool operator was unable to include this clause in his contract, he may set up a collar to lock his bunker prices into a particular range and ensure the contract maintains the same financial performance as it would have if the clause had been included.

Leave a Reply

Want to join the discussion?Feel free to contribute!